EnviroForensics’ Second Environmental Science Education workshop introduces Herron High School’s AP environmental science students to the daily operations of environmental scientists, real-world scientific applications of concepts learned in the classroom and helpful advice on pursuing a degree and a career in the environmental field. The workshop includes hands-on presentations covering topics like chemical properties of typical contaminants, fate, and transport of contaminants in the environment, and investigation and cleanup techniques. The objective is to give students some perspective on how the lesson they’re learning inside the classroom can apply to their future careers. The workshop is hosted in the Field Lab where EnviroForensics personnel and interns come to learn the basics of environmental field sampling or brush up on their own skills.

Presentations Covering topics like: Groundwater and Soil, Vapor Intrusion, Remediation Technologies, Site Redevelopment, Risk Communication, and Education Requirements for the job.

Herron High School is a public charter college preparatory schoollocated in downtown Indianapolis providing classical and liberal arts-based education (math, English, science, social studies, Latin, music, performing arts and visual arts) and serves more than 700 students grade 9-12 of varying cultural and socioeconomic backgrounds.

The workshop is led by Casey McFall, Director of Field Services at EnviroForensics.

Special thanks to all the people who made today special: Casey McFall, Collin Martin, Morgan Saltsgiver, Matt Bono, Brianne Inman, Grace Randall, and Stephen Henshaw.

LEARN HOW OLD INSURANCE POLICIES CAN BE USED AS FUNDS TO PAY FOR ENVIRONMENTAL INVESTIGATION, REMEDIATION AND LEGAL COSTS.

BY: STEPHEN HENSHAW & DAVID O’NEILL

Once I met with a dry cleaner who said he had gone to the attic in search of his old business package policies. He explained that he had no idea before visiting an attorney that these old expired insurance policies could be of any use to him. Since they were package policies, they contained multiple lines of insurance. Parts of the policy provided coverage against damage to his building, against break-ins, storm damage and even workers compensation coverage. As far as he knew all of this coverage had long ago expired. Why would he still have copies of these old policies? There was no reason, he thought, that he would want to have kept them. They would have to be in a box or two that he had neglected to put in the dumpster.

LEARNING THE VALUE OF OLD COMMERCIAL GENERAL LIABILITY POLICIES IN ENVIRONMENTAL CLEANUPS

He had been told by his attorney to look for that part of the policy that addressed damage to the property of others. Not damage to others he might do in his delivery van. That was covered under the automobile insurance section of the policy. Rather, it was the part of the policy that covered his customers (the slip and fall coverage) that he was looking for. His attorney had told him that part of the old package policies could provide him the coverage he needed now to address the environmental contamination on his property from perchloroethylene (Perc) spills below ground that had occurred years earlier.

THE IMPACT OF PERC SPILLS WHEN REFINANCING A PROPERTY

It was these Perc spills that apparently had caused all the trouble. The landlord, a strip mall owner, had been refinancing and the bank required that he conduct a simple environmental audit that had included soil sampling. The samples had shown Perc in the soil at his end of the strip mall. The landlord was going to have to clean this up to get his refinancing. The cleanup would be expensive and the dry cleaner was expected to take care of the bill because he was the one who had accidentally put the Perc into the soil over the many years of his operation there. The attorney had assured the dry cleaner that this was indeed legal. The law in his state required that “the polluter” remove the pollution or at least reimburse the landlord if he had to have it done. Up until this time, the dry cleaner had not considered himself a polluter–it was a new role he was going to have to get used to before this nightmare would be over.

UTILIZING OLD CGL POLICIES TO FUND ENVIRONMENTAL CLEANUP

His attorney had explained that in his state, as in most states, it took policies issued before 1986 to pay for environmental investigations. This was because the later policies contained pollution exclusions that the courts in his state recognized as barring coverage for Perc spills. Paying the landlord’s environmental experts was likely to be too great for the dry cleaner to handle. After years of operating a successful business, he had significant savings, but these ongoing costs could deplete that savings account in no time. He may even need to consider bankruptcy unless he could find those insurance policies issued before 1986, and successfully file claims that would require his insurers to step in and defend him.

Digging around in the attic, he succeeded in finding one collection of old policies, but these policies dated only to the late 1990s. Telephoning the insurance agent identified on the policies, the dry cleaner found that that insurance agency was no longer in business. Despairing, he reported his lack of success to the attorney, prepared to discuss bankruptcy instead of insurance recovery. However, the attorney suggested another option. He suggested that the dry cleaner hire an insurance archeologist to see what insurance might be located elsewhere.

Dave O’Neill, JD, Director of Investigations at PolicyFind, reviews historical policies.

Working backward from the earliest insurance policy, the insurance archeologist was able to discover that another insurance agency had purchased the defunct agency’s book of business prior to closing.

Contacting that insurance agency, the archeologist found that old policy files no longer existed, but that the agent would permit him to review his old accounting files. A review of these files identified some premium notices issued to the dry cleaner in 1985. These notices identified the policy numbers, dates and insurance carrier.

The insurance archeologist provided a specimen policy issued by the same insurance carrier to a different dry cleaner in his state from the 1985 policy period. This policy had a pollution exclusion on it but that exclusion, the attorney advised, was not a bar to coverage as long as the Perc releases had not been intentional, and had been “sudden and accidental.”

Using the premium notices and specimen policy together, the dry cleaner’s attorney was able to file a claim with the insurance company. The company stepped in to defend the dry cleaner, paid his attorney fees and paid the landlord’s environmental experts.

THE MORAL OF THE STORY

Don’t give up. Get some professional help and look under every rock. Ask your attorney about how insurance archeology can help you locate the records you need to defend against environmental claims.

Stephen Henshaw, Founder at EnviroForensics & PolicyFind has over 30+ years of experience and holds professional registrations in numerous states. Henshaw serves as a client manager and technical manager on complex projects involving contaminated and derelict properties, creative litigation, deceased landowners, tax liens, non-performing banknotes, resurrecting defunct companies and cost recovery. Henshaw’s expertise includes a comprehensive understanding of past and current industry and waste handling practices and the fate and transport of chlorinated solvents in soil and groundwater. He has served as a testifying expert for plaintiffs and defendants on high profile cases involving causation and timing of releases, contaminant dispersion, allocation, damages, past costs, and closure estimates. He has a strong knowledge of state and federal regulations, insurance law, RCRA, and CERCLA. He has managed several hundred projects including landfills, solvent and petroleum refineries, foundries, metal plating shops, food processors, dry cleaners, wood treating facilities, chemical distribution facilities, aerospace manufacturing facilities, and transporters and provides strategy instrumental in funding projects and moving them to closure.

David O’Neill, JD, Director of Investigations at PolicyFind has 30+ years of experience in claims recovery on behalf of corporate policyholders involving environmental property damage and toxic tort and asbestos exposure claims. O’Neill has extensive experience in locating and retrieving insurance coverage evidence on behalf of potentially responsible parties responding to environmental investigation and remediation demands. His former investigative work includes unique matters involving Holocaust victims rights, mergers & acquisitions of a national landfill operator, and on matters involving national archives.

Insurance archeology solves funding issues for a dry cleaner who was distressed by the lack of effectiveness of his state’s environmental response fund.

This is the story of a Wisconsin dry cleaner who wanted to retire, but his property was plagued with environmental contamination and funding challenges despite his enrollment in Wisconsin’s Dry Cleaner Environmental Response Fund (DERF). Here’s how he found a way to get his unsellable property clean and ready for redevelopment.

The Discovery of PERC Contamination

The dry cleaner was in operation from 1968-2001 and throughout that time tetrachloroethene (PERC), a dry cleaning chemical, was used to clean its customers’ clothes. PERC became a common dry cleaning chemical in the 1930s and is now less frequently used in dry cleaning operations due to concerns for worker health and the environment.

Engaging the DERF

In 2001, the dry cleaner decided to retire and utilize the Wisconsin DERF so he could sell his business. The fund was contributed to through a license fee and a solvent fee by dry cleaners. Luckily, the dry cleaner owner contributed to the DERF program while in business and was eligible to utilize the funds for his investigation and remediation.

In hopes of selling his dry cleaning business to a buyer, he had to conduct an initial environmental investigation to begin the environmental due diligence process and gain access to his DERF reimbursements.

Working with the State’s Environmental Response Trust Fund

From 2002-2011, the dry cleaner paid for his clean up activities out-of-pocket while waiting for his reimbursements to come through from the DERF program. He contracted an environmental firm to conduct Phase I and Phase II Environmental Site Assessments (ESA), but the environmental firm’s work was constricted to a very slow pace due to the slow payments from DERF.

By 2014, the dry cleaner was well into his retirement and was no longer running his business, but he still needed to clean up the environmental contamination in order to sell the property. After spending roughly $250,000 out-of-pocket for his environmental investigation and remediation work, he had completely run out of personal funds. He could no longer pay for any additional work upfront and he could no longer wait on reimbursements from DERF.

Contacting local dry cleaning association for help

After the frustration the dry cleaner experienced with the DERF program, he contacted the Wisconsin Fabricare Institute (WFI), part of the national Drycleaning and Laundry Institute (DLI), for help on how to get him through this predicament. WFI recommended contacting EnviroForensics and its insurance archeology division, PolicyFind to find alternative funding sources.

Engaging with EnviroForensics

PolicyFind conducted insurance archeology to locate the dry cleaner’s old insurance policies. They evaluated the dry cleaner’s historical commercial general liability (CGL) policies and developed an insurance claim strategy to access funding that could be used to complete the environmental investigation and remediation–so he could finally sell his property.

To recap, in order to solve the dry cleaner’s financial challenges, PolicyFind:

Tendered the insurance claim with the insurance carrier, which led to the carrier confirming that the insurance would pay for the environmental work.

The switch from using DERF funds to historical insurance coverage to pay for the environmental work allowed the dry cleaner to finally clean up his property, which was a precursor for being able to sell his property.

The environmental investigation and remediation process

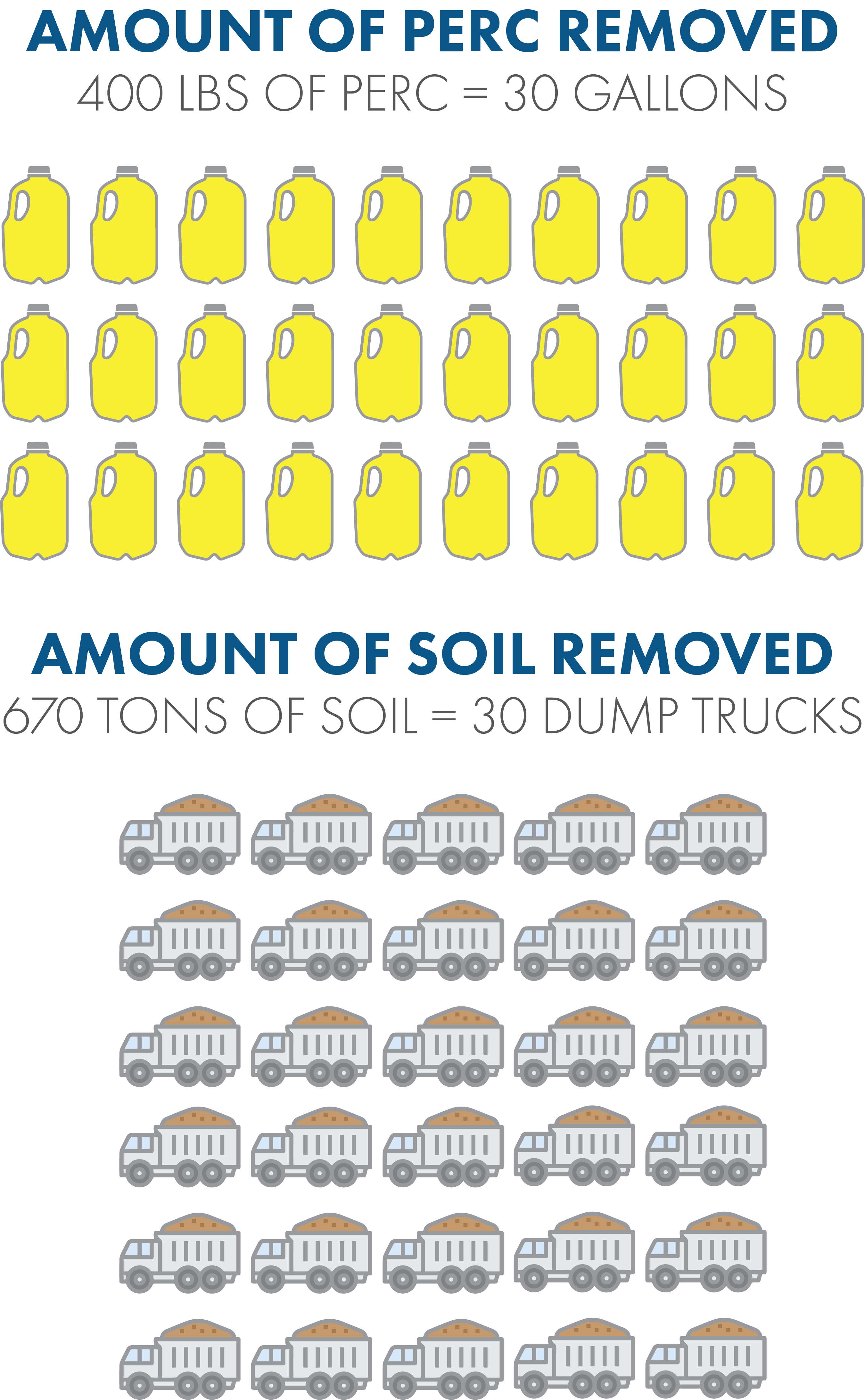

Once the insurance archeology funds were secured, EnviroForensics completed the remaining site investigation activities which included soil and groundwater delineation as well as vapor intrusion assessments. The results showed that there was soil contamination, which required additional remediation to gain site closure. Geologists and engineers developed a remediation plan to demolish the building and remove the existing contamination. EnviroForensics conducted a soil excavation and removed approximately 400 pounds of PERC and 670 tons of contaminated soil.

The amount of perc and contaminated soil from one dry cleaner is shown in the above two graphics. It’s astonishing to see the physical evidence from three decades of small and accidental releases of perc from a dry cleaner.

After the remediation, EnviroForensics completed a Phase I ESA to prepare the property for resale and helped the former dry cleaner find an investor to purchase the property, who took on the remaining environmental liability, which included ongoing environmental monitoring.

EnviroForensics helped find a buyer

Since the majority of the environmental work was complete and the CGL insurance policies had enough funding for the ongoing environmental monitoring, the investor felt comfortable working with EnviroForensics to settle the environmental claim and continue cleaning up the property.

Map overview of the former dry cleaner in Appleton, Wisconsin.

A New Life for the Property

The ongoing site work facilitated the sale of the property and future redevelopment plans are underway for potential reuse as a commercial office building.

The former dry cleaner site is nearing the end of its investigation and remediation work. The closure of the site, under the Wisconsin Department of Natural Resources (WDNR), is anticipated after minor investigation follow-up activities and continued environmental monitoring by 2021.

EnviroForensics® is a full-service environmental consulting firm that has cleaned up more dry cleaning sites than any other firm. We’re the only firm that focuses on finding the money to pay for investigation, cleanup, and legal fees. We restore the value of your property while protecting you from regulatory and legal issues.

We talk a lot about environmental investigations and the types of important decisions that dry cleaners need to make during the environmental cleanup process. Some dry cleaners have dealt with the environmental investigation and remediation process before, and others haven’t had to deal with it up to this point. For those of you who haven’t yet become a reluctant expert in the field, it’s helpful to consider some entry-level investigation concepts.

Understanding The Environmental Investigation Process in 3 Steps

In recent articles, we’ve discussed the difference between Phase I and Phase II investigations, and that they are a part of a systematic approach to determining if the potential exists for environmental contamination during a commercial real estate property transaction.

Key terms:

A Phase I Environmental Site Assessment (ESA) is the due diligence evaluation that addresses the past land uses of a property or group of properties and identifies the potential for environmental concerns to be present.

A Phase II ESA generally includes an initial or preliminary subsurface investigation, with sample collection, to determine whether or not the soil, soil gas or groundwater beneath the subject site is contaminated with metals, petroleum hydrocarbons, chlorinated solvents or other chemicals of concern, based on the past land uses identified in the Phase I.

A Nature and Extent (N&E) Investigation is performed if, during the Phase II ESA, contamination is detected in soil, soil gas or groundwater samples. When a regulatory agency conducting oversight (for example, the Regional Water Quality Control Board, the California Department of Toxic Substances, or local county agencies) requires the responsible party to fully remediate the contamination, they will first require that the responsible party get their arms around the magnitude of the problem in its entirety.

For dry cleaning sites, defining the Nature and Extent of the contamination is often tackled in a series of several steps.

STEP 1: Determine how far the contamination has spread away from the likely source area(s) laterally. Source areas are the location(s) where dry cleaning solvents first entered the subsurface. We commonly see that these source areas are the location of the existing and former dry cleaning machines, the waste storage areas, and the sewer system, but can also include storm drain systems, delivery bays or roof downspouts.

This graphic is an example of a source area with a subsurface view from a dry cleaning business.

The thing to remember about source areas at dry cleaning facilities is that the area where the release to the soil and groundwater occurred can be relatively small as compared to the size of contamination plume overall. This can make finding the source difficult. If you’ve hired an experienced consultant using the tips I gave you in last month’s “5 Considerations When Selecting an Environmental Consultant”article, you have a better chance of success in this effort.

STEP 2: Determine how deep the contamination has migrated. In cases where the groundwater table is very deep, the contamination found in the soil may not have reached that far down. If that is the case, consider yourself lucky because once a chlorinated solvent plume reaches the groundwater it can migrate pretty far away from the source.

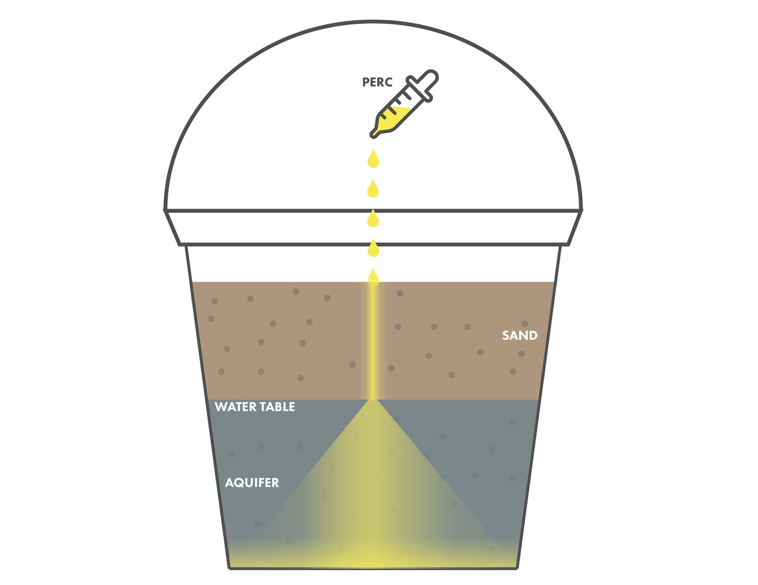

Let’s talk about how groundwater plumes move. Sometimes when I teach people about the presence of groundwater and how it moves in the subsurface, they get a vision of an underground lake or river. That’s not it at all. Probably the best way to imagine groundwater is by visualizing a bucket of dry sand. That sand represents the subsurface geologic materials (rocks, sediments) beneath your dry cleaner.

Illustration of perc creating a common pathway through the sand and down to the water in the bottom of the bucket.

Now, if you fill that bucket half-way with water, the portion of the sand that is saturated with water is equivalent to the “aquifer”, and the top of the saturated part of the sand is the “water table”. You can imagine that if a very small quantity of perc is dropped at the very top of the bucket of sand, it would quickly be absorbed by the dry sand and none of it would reach the water table below. If that small drop of perc is repeated time and time again, a larger portion of the dry sand would contain perc until at some point the perc would saturate a common pathway to reach the depth of the water table in the bucket. This is how many releases of perc can eventually reach the groundwater beneath a dry cleaner.

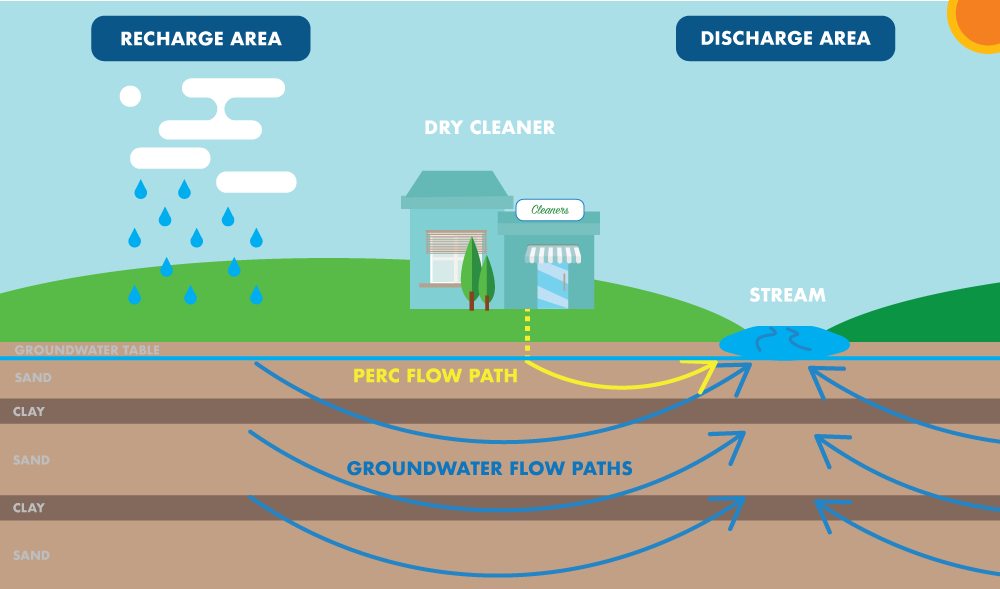

This graphic illustrates the concept below, which explains how groundwater moves away aquifers or “recharged” areas and moves towards areas where an aquifer “discharges” or loses water, such as streams.

If perc contamination has actually reached the groundwater, it will start to move along with the subsurface groundwater and will migrate at a rate that can be calculated. It is interesting to consider how and why groundwater moves. Conceptually, consider that groundwater moves away from areas where the aquifer is “recharged”, or takes on water, and toward areas where the aquifer “discharges” or loses water.

A simple way to demonstrate this is by visualizing a grassy field where rainwater seeps into the soil and adds water to the groundwater aquifer. This is a recharge zone. A common discharge zone is a stream some distance away, at a lower elevation, that receives a portion of its water from the groundwater table. So, in this scenario, groundwater would flow from the grassy field toward the stream. If a dry cleaner site has released PERC into the soil near the grassy field and the contamination plume makes its way down to the depth of the groundwater table, the perc could migrate to the stream as well. It’s certainly not a fast process, but since most dry cleaner releases are decades old, it’s possible. That is why environmental consulting firms hire licensed professional geologists and engineers who understand these types of processes.

STEP 3: If groundwater samples need to be collected, the cost-effective approach is to first collect “grab” samples. Grab samples are samples collected one time and at specific locations and depths. They provide an inexpensive snapshot of the groundwater quality. Grab samples are typically collected through a steel rod that has been advanced from a drilling rig or percussion drilling device. It is necessary to also collect appropriate quality control samples during the sampling activities.

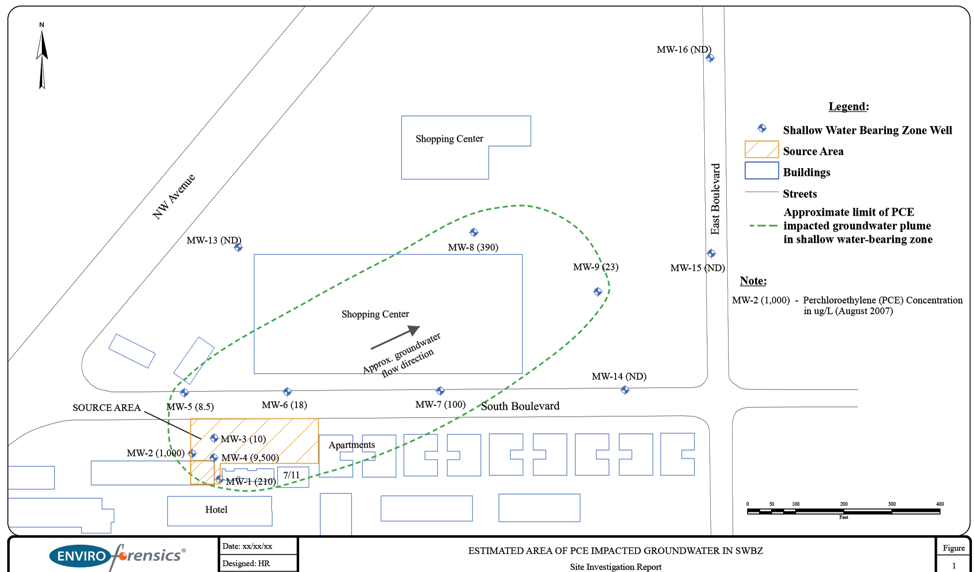

The sampling locations and sample results for both soil gas and groundwater samples are then placed on a map as shown in Figure 1 (below) and on a cross-sectional diagram, as shown in Figure 2 (below).

Figure 1 is a map that shows soil gas and groundwater sample locations.

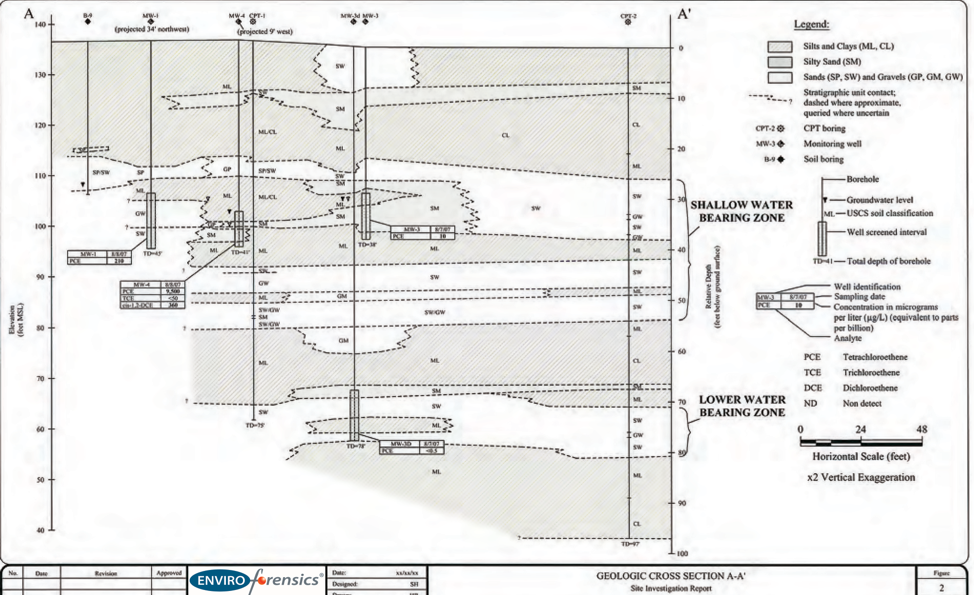

The cross-section (Figure 2) actually gives you a picture of the geological layers beneath the property and how far the contamination has spread laterally and vertically. If you haven’t yet had any exposure to the environmental investigation process, this is how your consultant will communicate the information to you and the regulators.

Figure 2 shows the cross-section of geological layers beneath the contaminated property, which includes soil and groundwater.

If groundwater has been impacted, you will be required to install permanent monitoring wells, from which groundwater samples can be collected over the course of a year or two to get a better understanding of the groundwater quality. Groundwater levels, or the depth of the groundwater table in each well, are also collected to determine the groundwater flow direction. Depending on how much rain is received during the measurement interval, the depth of the groundwater table moves up or down. Tests can also be conducted using the monitoring wells to develop an understanding of the hydraulic conductivity of the water-bearing unit. These results assist in determining the groundwater velocity and how fast the contaminated groundwater moves over time. While it may not be necessary to have the site fully characterized before implementing remedial activities, it is common to need these types of site characterization tests to design the appropriate remediation plan.

Next Steps for Your Environmental Investigation

These preliminary site investigation and characterization efforts can cost a lot of money and take several months to complete, not including long-term stewardship monitoring. It is not uncommon, however, for the responsible party to feel like things are happening way too fast, especially if they haven’t yet fully grasped the scientific basis of what is happening.

THE FABRICARE INDUSTRY DOESN’T HAVE IT EASY THESE DAYS. INDUSTRY CHANGES THAT ARE FORMING ON THE HORIZON WILL COME TO PASS–FASHION, INCOME, AGE, SOCIETAL TRENDS, AND DISRUPTIVE BUSINESS MODELS WILL CONTINUE TO SHAPE THE DEMANDS OF CUSTOMERS.

Dry cleaners will continue to evolve and adjust to the market just like they’ve done for over a century. If you’re one of the 33,000 dry cleaners in the United States, it can feel like trying times. But you’re not alone. In fact, you have a large community of dry cleaners–as evident by the 11,000 attendees at this year’s Clean Show–and resources at your fingertips.

From government resources and associations to publications and thought leaders, here’s a list of the top 10 resources available to dry cleaners.

1. NATIONAL AND REGIONAL DRY CLEANING ASSOCIATIONS

Here’s a few of the dry cleaning association logos.

Drycleaning & Laundry Institute International(DLI) is a membership-based organization aimed to empower drycleaning entrepreneurs and their staff to offer the best quality and customer service in the industry.

DLI has a network of thousands of dry cleaners. DLI’s blog regularly shares industry best practices on all dry cleaning and laundry topics from clothing drop off processes to removing stains, cleaning, finishing, and packaging. DLI also offers valuable business information including employee relations, hiring, firing, governmental and running a small business.

DLI’s School of Drycleaning Technology offers several courses throughout the year, online certification testing and renewals, and courses across the US.

Check out some of the associations available to dry cleaners throughout the U.S.

Cleaner and Launderer has been around since 1960. Originally, the publication was called “Western Cleaner & Launderer,” and served industry news and information to dry cleaners throughout California. Now, readership and distribution have grown exponentially with copies of the monthly edition landing in mailboxes across all 50 states. In 2007, the name was changed to “Cleaner and Launderer” as the brand expanded its reach in digital and social networks. Helpful articles in Cleaner and Launderer run the gamut from industry updates and employee morale tips to monthly columns, such as:

Word From the Street, where John Leano shares business management.

the Environmental Corner, where EnviroForensics’ Jeff Carnahan shares educational content on environmental contamination and cleanup, advice on addressing environmental liabilities, and tips for finding the funds to pay for environmental cleanups and legal fees

Show Your Customers Your Expertise, where Kenny Slatten provides textile treatment insights and tips.

The front page of Cleaner and Launderer’s July 2019 issue.

American Drycleaner is one of the leading dry cleaning publication in the country. Distributed in both print and digital format, the magazine boasts a wide variety of resources for both small and large dry cleaning business owners. Their mission is to help dry cleaners run their businesses better, with up-to-the-minute information on industry news, events and trends. Other valuable resources on their website include:

National Clothesline is a free publication for dry cleaners and is read by close to 20,000 cleaners and suppliers across the country and around the world. The newsletter provides news and information needed by garment care professionals to be successful in a rapidly changing industry. On the National Clothesline website, along with its digital edition, you will also find a “Resources” page that includes:

An online forum for dry cleaners

A directory of business consultants

A list of courses and seminars provided to dry cleaners

Books, DVDs, and other forms of helpful media

Government regulations for dry cleaners

The front page of the National Clothesline’s July 2019 issue.

5. FABRICARE MAGAZINE DLI publishes the Fabricare magazine on a quarterly basis and provides resources and education to dry cleaners. This magazine features educational, management and industry resources and covers topics like

As the dry cleaning industry’s most trusted environmental consultant, EnviroForensics’ Blog aims to empower dry cleaners with a host of helpful articles, educational content, and informative posts about the different issues, process and questions that dry cleaners encounter when they’re addressing their environmental liabilities.

PolicyFind is an insurance archeology firm that locates historical insurance policies for business and property owners, municipalities, attorneys and private equity firms. So, if you’re looking for your old insurance policies to help pay for an environmental investigation and cleanup, PolicyFind™, is a great resource. PolicyFind’s blog is a helpful resource, too, with educational content and case law updates.

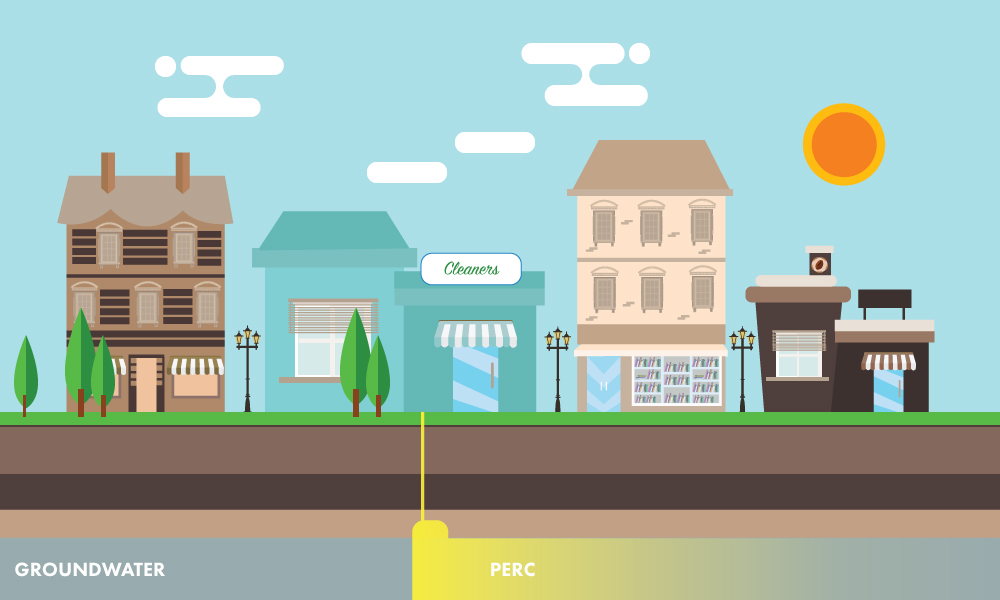

Environmental laws vary from state to state but ultimately echo the laws at the federal level. The United States Environmental Protection Agency has its guidance on common dry cleaning solvents like PERCposted to their website, alongside thousands of peer-reviewed studies and other archives.

The EPA’s webpage on tetrachloroethylene (Perc, PCE).

9. UNITED STATES DEPARTMENT OF LABOR: OSHA REGULATIONS FOR DRY CLEANERS It’s important for dry cleaners to up to date on occupational safety and health. The Occupational Safety and Health Administration (OSHA) has it’s set standards for dry cleaners along with resources for hazard recognition on their website as a resource for dry cleaners.

The OSHA standards resource webpage for dry cleaners.

10. SMALL BUSINESS OWNER MARKETING TOOLS Drycleaners are small business owners and they have to run an entire business while maintaining their drycleaning operations. It’s a lot to handle and it isn’t for the faint of heart. How can drycleaners keep up with the digital demands on small business owners? They can use marketing tools to help get the word out about their business and share their unique selling points in a way customers will want to engage with your business.

Wix and Squarespace are helpful for website development and management.

Mailchimpis a great tool for email marketing. You can update your clients on discounts, news or best practices for taking care of their clothes.

Canva is an easy graphic design tool for social media graphics, posters, flyers, and brochure templates.

Hootsuite and SproutSocial are good tools for social media scheduling and management.

Some Funds are either running out of money or have already sunset. What is the dry cleaning industry turning to for the money needed to respond to environmental liability? Dry cleaners are increasingly using their historical insurance policies to pay for environmental cleanup claims—protecting their business from financial ruin or bankruptcy.

The dry cleaning industry has seen more than its fair share of costly and complicated environmental contamination issues. In the past, eligible dry cleaners in almost 25% of the United States have been able to use money from state trust funds that were established solely for this purpose. Unfortunately, these state trust funds have proven to be not sustainable in most situations, and the number of available funds is declining. In the coming years, it’s anticipated that those looking to the state fund programs will experience even more delays in reimbursement of money already spent out-of-pocket, and or will lose the fund altogether.

Who is potentially impacted by this news? Any dry cleaner in Alabama, Connecticut, Illinois, Florida, Kansas, Missouri, North Carolina, Oregon, South Carolina, Tennessee, Texas, or Wisconsin.

This is frightening news for dry cleaners in these states, who are liable for cleaning up environmental contamination caused by cleaning solvents like PCE (Perc) or TCE. However, another financial solution is still available to dry cleaners—their historical Commercial General Liability (CGL) insurance policies. By finding their historical insurance policies, dry cleaners can use them as assets to help pay for their environmental investigation and cleanup. Those residing in states without trust funds have been doing it for years.

How Can Dry Cleaners Use Historical Insurance Policies to Pay for Environmental Cleanups?

Historical insurance policies are valuable assets that you can use to get money to pay for resolving environmental issues.

Commercial general liability (CGL) policiesprovide coverage to businesses for bodily injury, personal and property damage caused the business’ operations, products, or injury that occurs on the business’ premises. Most every business has old CGL policies since they are commonly purchased as a necessity to cover potential costs incurred by defending and reasonably resolving suits seeking to hold them liable for alleged bodily injuries or property damage.

Historical Commercial General Liability (CGL) policies from before 1985-86 typically don’t have a clause that disallows coverage for releases of contaminants. This means that if a dry cleaner can find their or their predecessor’s old insurance assets, then those policies can pay for the environmental investigation and cleanup required by the state’s environmental regulatory agency. Additionally, the policies would likely protect dry cleaners from any neighbors who decide to sue them for damage to their property. These policies also entitle dry cleaners to hire an environmental defense attorney at no charge and receive insurance payments immediately without upfront payments, unlike most state trust funds.

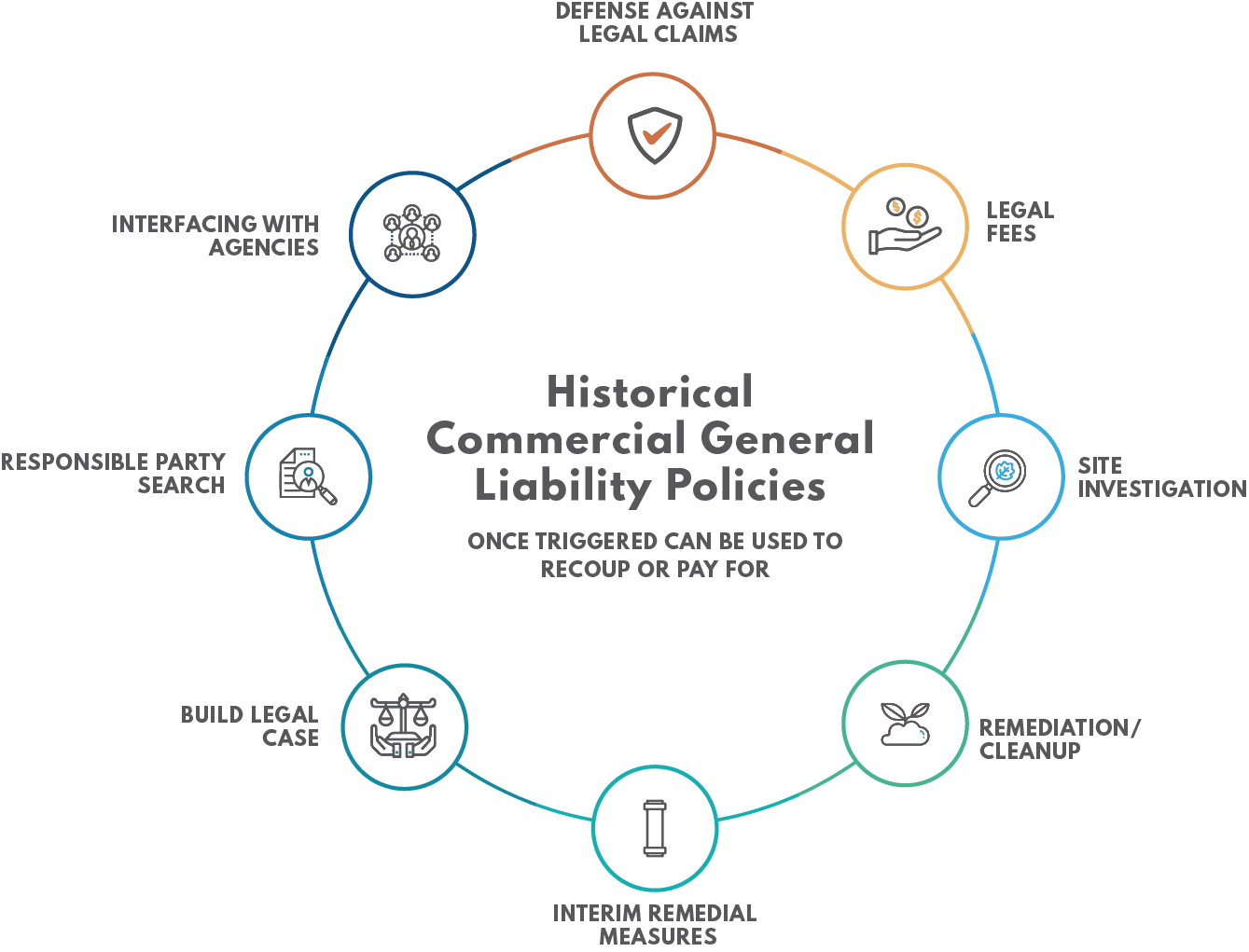

Once triggered historical commercial general liability (CGL) policies can be used to recoup or pay for 1) site investigation, 2) remediation/cleanup, 3) interim remedial measures, 4) building a legal case, 5) responsible party search, 6) interfacing with agencies, 7) defense against legal claims, and 8) legal fees. To learn more about CGL policies, visitHow Does It Work? CGL Policies and Insurance Archeology.

How Do You Find Old Insurance Policies?

Insurance archeologists conduct insurance archeology to find lost or misplaced liability insurance policies that can defend and indemnify policyholders against claims such as environmental property damage claims.

EnviroForensics® is the nation’s leader in finding and using historical insurance coverage. Our insurance archeology division, PolicyFind™, has decades of experience identifying and locating lost, mislaid, or destroyed liability insurance policies for policyholders.

First, insurance archeologists retrace the genealogy of historical insurance coverage to identify past owners and operators who may have contributed or caused personal injury or environmental damage.

Next, they use an extensive specimen policy library to help confirm terms and conditions, research data services, and physical file searches to follow leads and locate evidence of old insurance policies.

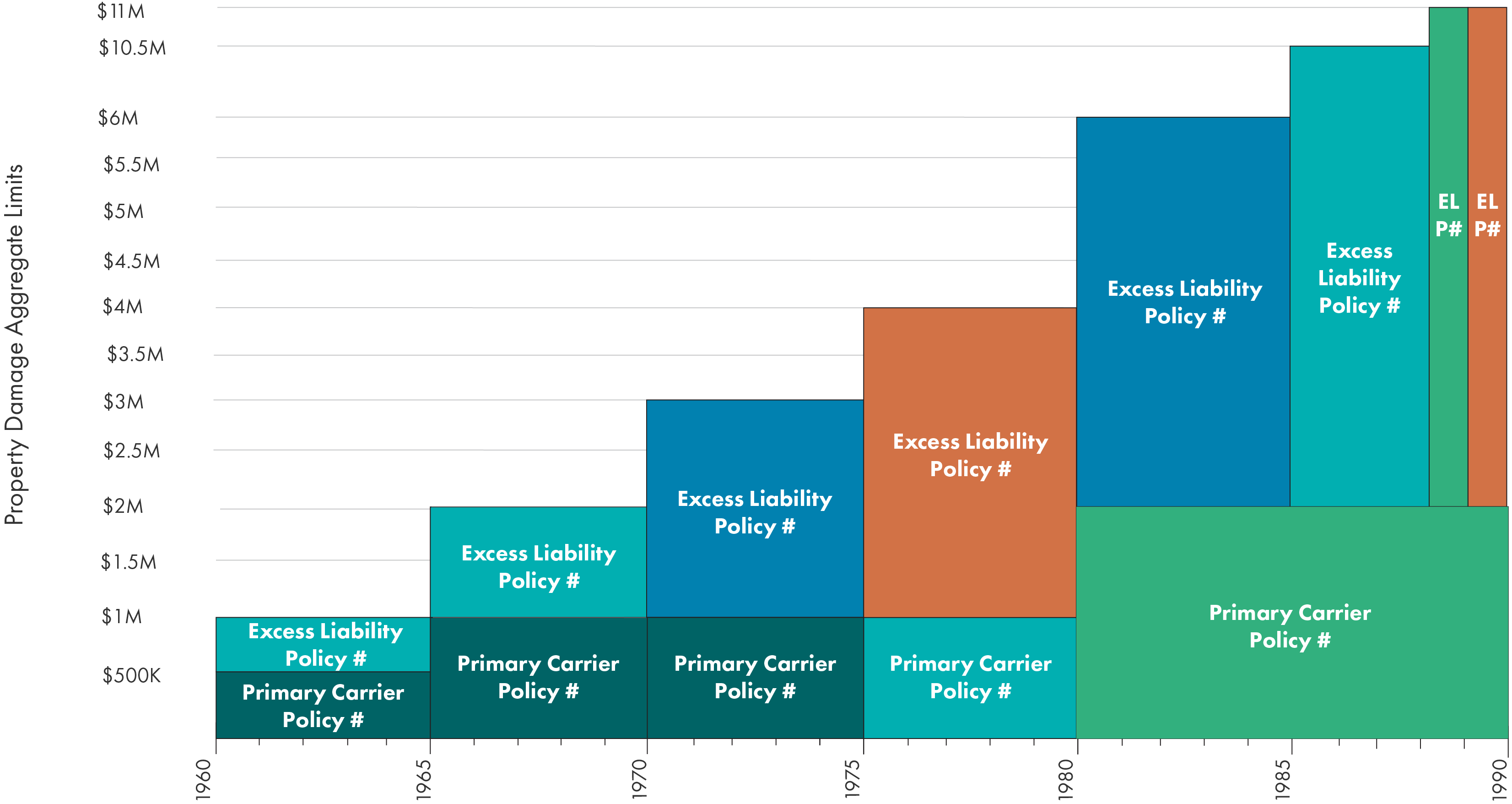

And finally, the results of the insurance archeology process are assembled into insurance coverage charts, which visually reconstruct the CGL insurance policies.

This is an example of a typical Insurance Coverage Chart that has reconstructed historical insurance policies from 1960 to 1990. The policies include general liability policies and excess/umbrella liability policies. This particular coverage shows property damage aggregate limits per policy period and what carriers are liable for from the policyholder’s coverage period.

The rebuilding of historical land use and insurance can limit the liability of individual clients. Initiating coverage from these policies thereby creates an alternative funding source, which can protect a business from severe financial loss and even save a company from bankruptcy.

“If historical insurance policies are lost or misplaced, PolicyFind’s expert insurance archeologists will find the needed evidence of their existence and create a legally defensible historical insurance coverage chart—saving a dry cleaner’s livelihood,” says President of EnviroForensics.

Once identified and brought to light, the coverage provided by old insurance policies can be used to hire an environmental consulting firm with specialized expertise in serving the dry cleaning industry by cleaning up its historical environmental pollution problems.

How EnviroForensics Can Help

EnviroForensics® is the nation’s leading environmental engineering firm serving dry cleaners. EnviroForensics is the only full-service environmental firm that performs insurance archeology to locate money to pay for environmental investigation, cleanup, and legal fees. EnviroForensics helps clients get their cleanups paid for without significant cost to the clients or their businesses while restoring their property to fair market value.

Commercial General Liability (CGL) Policies protect your business from financial loss should you be liable for property damage or personal injury caused by your services, business operations or your employees. CGL policies are sometimes referred to as “slip and fall policies” or “everyday business insurance” because they provide liability insurance coverage for general business risks.

What Does Historical Commercial General Liability Insurance Cover?

Historical CGL policies, once located and leveraged, typically cover the costs of your legal defense and will pay on your behalf of damages if you are found liable—up to the limits of your policy. CGL coverage is important due to the negative impact that a lawsuit can have on your business and because liability suits can happen so frequently.

Insurance companies have a duty to defend, which means they’re obligated to provide the insured policyholder with defense against claims made under a liability insurance policy. As a general rule, the insured policyholder needs only to establish that there is potential for coverage under a policy to begin the process for the insurance carrier’s duty to defend.

Why are Historical Commercial General Liability Policies Valuable?

You or your predecessor’s historical CGL policies are valuable assets because you can use the policies to pay for resolving environmental liabilities.

Facts about CGL Policies

CGL policies insure business owners against claims for property damage like environmental contamination and bodily injury.

CGL policies written prior to 1985-86 have a clause that creates an exception for “sudden and accidental” releases of contaminants.

Applicable CGL policies never expire.

Older CGL policies can cover long-tail claims, such as environmental investigation, cleanup, and legal counsel fees.

Old CGL policies are still valuable even if a company is bankrupt or a former owner is deceased.

Once triggered historical commercial general liability (CGL) policies can be used to recoup or pay for 1) site investigation, 2) remediation/cleanup, 3) interim remedial measures, 4) building a legal case, 5) responsible party search, 6) interfacing with agencies, 7) defense against legal claims, and 8) legal fees. To learn more about CGL policies, visitHow Does It Work? CGL Policies and Insurance Archeology.

Depending on your situation and the state in which you conduct business, the out-of-pocket environmental cleanup costs may be minimal. This is why historical CGL policies are valuable assets that may be worth millions of dollars.

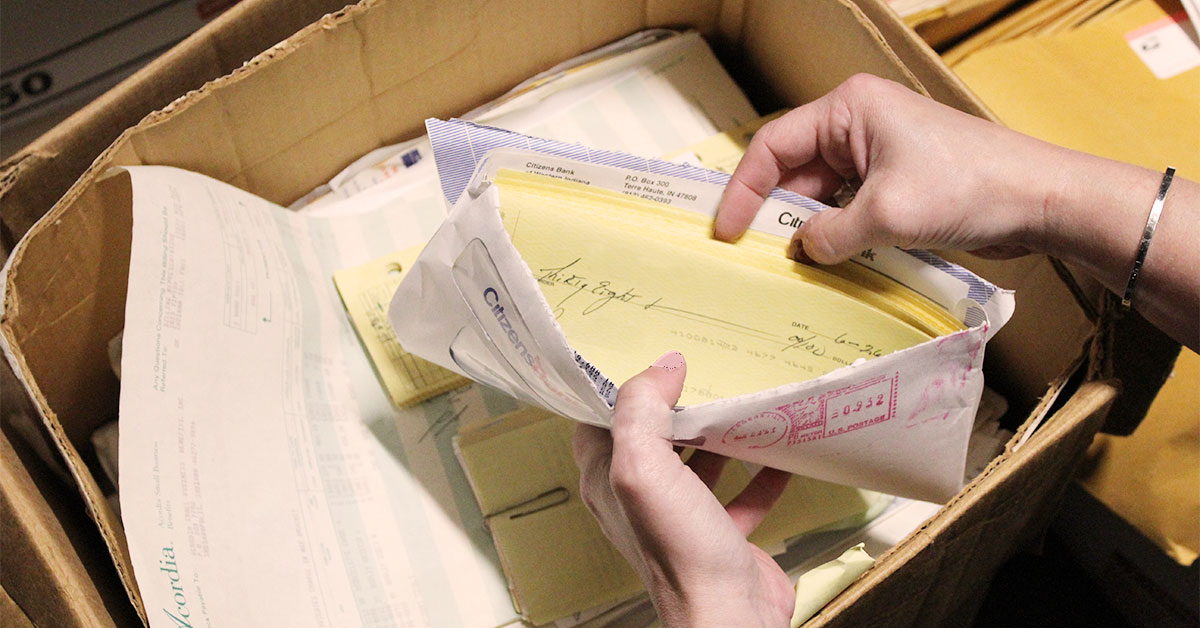

An insurance archeologist searches old file boxes in a company’s basement.

Biggest Tips for Proving Historical CGL Coverage

Keep everything! Many types of old records can result in leads, which could assist your insurance archeologist in locating valuable insurance assets. Sometimes what seems to be irrelevant is actually very valuable.

Hire an insurance archeologist. Insurance policies are complex contracts between the insured policyholder and the insurance carrier, which requires a trained eye to interpret and understand the nuances of case law.

Stephen Henshaw, Founder at EnviroForensics & PolicyFind has over 30+ years of experience and holds professional registrations in numerous states. Henshaw serves as a client manager and technical manager on complex projects involving contaminated and derelict properties, creative litigation, deceased landowners, tax liens, non-performing banknotes, resurrecting defunct companies and cost recovery. Henshaw’s expertise includes a comprehensive understanding of past and current industry and waste handling practices and the fate and transport of chlorinated solvents in soil and groundwater. He has served as a testifying expert for plaintiffs and defendants on high profile cases involving causation and timing of releases, contaminant dispersion, allocation, damages, past costs, and closure estimates. He has a strong knowledge of state and federal regulations, insurance law, RCRA, and CERCLA. He has managed several hundred projects including landfills, solvent and petroleum refineries, foundries, metal plating shops, food processors, dry cleaners, wood treating facilities, chemical distribution facilities, aerospace manufacturing facilities, and transporters and provides strategy instrumental in funding projects and moving them to closure.

Stephen Henshaw, Founder at EnviroForensics & PolicyFind has over 30+ years of experience and holds professional registrations in numerous states. Henshaw serves as a client manager and technical manager on complex projects involving contaminated and derelict properties, creative litigation, deceased landowners, tax liens, non-performing banknotes, resurrecting defunct companies and cost recovery. Henshaw’s expertise includes a comprehensive understanding of past and current industry and waste handling practices and the fate and transport of chlorinated solvents in soil and groundwater. He has served as a testifying expert for plaintiffs and defendants on high profile cases involving causation and timing of releases, contaminant dispersion, allocation, damages, past costs, and closure estimates. He has a strong knowledge of state and federal regulations, insurance law, RCRA, and CERCLA. He has managed several hundred projects including landfills, solvent and petroleum refineries, foundries, metal plating shops, food processors, dry cleaners, wood treating facilities, chemical distribution facilities, aerospace manufacturing facilities, and transporters and provides strategy instrumental in funding projects and moving them to closure. David O’Neill, JD, Director of Investigations at PolicyFind has 30+ years of experience in claims recovery on behalf of corporate policyholders involving environmental property damage and toxic tort and asbestos exposure claims. O’Neill has extensive experience in locating and retrieving insurance coverage evidence on behalf of potentially responsible parties responding to environmental investigation and remediation demands. His former investigative work includes unique matters involving Holocaust victims rights, mergers & acquisitions of a national landfill operator, and on matters involving national archives.

David O’Neill, JD, Director of Investigations at PolicyFind has 30+ years of experience in claims recovery on behalf of corporate policyholders involving environmental property damage and toxic tort and asbestos exposure claims. O’Neill has extensive experience in locating and retrieving insurance coverage evidence on behalf of potentially responsible parties responding to environmental investigation and remediation demands. His former investigative work includes unique matters involving Holocaust victims rights, mergers & acquisitions of a national landfill operator, and on matters involving national archives.